Capitalism has been blamed, by Piketty (2014) and many other economists, for increasing “wealth inequality” observed today. For example, Piketty (2014, p.23) suggested that the top decile of earners in the United States increased their share of income from 35 percent in 1980 to 50 percent recently, is the result of capitalism. However, without clearly defining what is meant by capitalism, the causal attribution has little logical foundation. Capitalism needs to be defined.

A previous post on “Capitalism and economic growth” has clearly defined capitalism as follows:

Capitalism refers to an economic system which allows individuals privately to own and use capital.

Under capitalism, wealth inequality should be expected, because some people work harder, save more, invest more and manage their finances more prudently than others. It takes a prejudiced mind to think that this source of wealth inequality is wrong, unfair or iniquitous. The alternative to this type of wealth inequality is equality in universal poverty, because otherwise there would be no incentive to work or produce.

Inequality vs Inequity

Of course, in typical muddled thinking, the “wealth inequality” which is deplored and discussed widely, is confused with “wealth inequity”. That is, what many are complaining about is actually not wealth or income inequality, which is really not the issue. Why should a doctor be paid the same as a janitor? Such equality would be iniquitous. The complaints are actually about wealth inequity which is wealth accrued unfairly from unprosecuted crime or from fraud or corruption in a rigged system.

Wealth inequity becomes self-evident sometimes when wealth inequality becomes excessive. In Piketty’s example cited above, he was probably suggesting that the US trend of increasing disparity of income may have become excessive. According to Oxfam, 82 percent of the wealth generated in 2017 went to the richest one percent of the global population, of which the poorest half or 3.7 billion people got nothing.

A corporate chief executive earning ten times more than the average of its employees may be at a level of income inequality which may not be regarded as unfair, but at a thousand times, many would suspect that it is excessive indicating inequity. What many economists fail to express accurately is the notion of unfairness, which does not exist generally in economics, especially not in mainstream economics which assumes efficient markets and rational individuals. The real problem is actually “wealth inequity” which may be defined as:

Wealth inequity is wealth inequality where the disparity in wealth is unfair, being disproportionate, or unrelated, to effort, productivity or contribution to society.

It is very important to draw the distinction between inequality and inequity because the solution to wealth inequality is wealth equality, which is the solution administered by socialist governments to eliminate wealth inequality. The imposition of wealth equality comes from, or leads to, socialism or communism, but it does not achieve fairness or wealth equity. The solution of wealth equity must come from an understanding of the origins of unfairness, not to be confused with socialist equality. In economics, the opposite of a wrong is another wrong; economists are forced to choose among wrongs – equality or inequity. Without a notion of fairness, in choosing to accept wealth inequality, most mainstream economists have also implicitly accepted inequity – gross and unfair inequality.

Indeed, the wealth inequality between countries depends dramatically on governments and their economic policies. Socialist countries are among the poorest in the world. For example, Venezuela has the highest oil wealth per capita, yet socialism under Hugo Chavez and continuing under Nicolas Maduro has transformed Venezuela from one of the richest countries in South America to a country racked with hyperinflation, poverty and even starvation – equality in misery.

Conversely, after Deng Xiaoping allowed China to run a market economy, confining its government largely to political matters, the Chinese economy boomed, converting socialist equality in poverty to capitalist inequality in wealth. No doubt, there has also been developing in China wealth inequity which is the subject of the rest of this post.

Inequity from Plunder

Wealth inequity is a threat to capitalism and should not be blamed on capitalism. The origins of wealth inequity have been identified centuries ago in the time of the American Independence and the drafting of the US Constitution. In a watershed era for mankind, the concept of human rights and ideas of good governance were intensively discussed and debated over a few decades. Among the writings of that era was “An Inquiry into the Principles and Policy of the Government of the United States” in which John Taylor of Caroline (1814, p.174) observed:

There are two modes of invading private property; the first, by which the poor plunder the rich, is sudden and violent; the second, by which the rich plunder the poor, slow and legal. One begets ferocity and barbarism, the other vice and penury, and both impair the national prosperity and happiness, inevitably flowing from the correct and honest principle of private property.

It is clear that plunder is a threat to capitalism which respects “the correct and honest principle of private property”. To paraphrase this astute observation on the origins of wealth inequity:

The rich plunder the poor slowly and legally, while the poor plunder the rich suddenly and violently.

The wealth inequality occurring through any form of plunder is wealth inequity because it is “unfair, being unrelated to effort, productivity or contribution to society”. Dishonest greed has been confused with capitalism. Today’s wealth inequality has resulted from decades when “the rich plunder the poor slowly and legally” – a form of dishonest greed, which contradicts honest private property and capitalism. Recent examples of this will be given below.

One form of plunder leads to its reverse form of plunder which, in this case, is when the poor plunder the rich suddenly and violently, as in a revolution. The most famous was the 1917 October revolution which led to the first communist dictatorship in the former Soviet Union. This and other socialist revolutions did not end well, because wealth equality is fundamentally unfair and led eventually to universal poverty in most cases.

Plunders of any sort victimize those who actually own and produce most of the wealth and are the honest working people in the middle which is the heart of capitalism. It is plunder, not capitalism, which causes today’s wealth inequity, manifested in gross and unfair inequality. There would be greater wealth equity and much less wealth inequality, if there were less plunder. The plunder in revolutions is easy to see, whereas the plunder in normal times is slow and legal, so it is hard to see and has been confused with capitalism.

Systemic Plunder

The global financial crisis (GFC) was, and still is, a blatant example of systemic plunder when the rich financial services industry plunders the rest of society. It was endogenous to the system through the application of wrong economic theories and policies (Sy, 2012). The GFC and other financial crises have been used as instruments of systemic plunder where

Systemic plunder is plunder which is legally enabled by a rigged system.

An example of systemic plunder is the actions of the investment bank, Goldman Sachs (GS) which Matt Taibbi (2009) described as follows:

The world's most powerful investment bank is a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.

A couple of well-known examples, involving GS, include the bankruptcy of Greece and the US sub-prime mortgage debacle, which deserve brief repetition here. First, before the GFC, GS helped corrupt officials to hide Greek government debt using off-market swaps, making hundreds of millions for GS in engineering those deals. The ballooning government debt eventually bankrupted Greece which was then rescued by the European Union only under punitive terms for the Greek economy.

Second, in the United States, GS packaged junk mortgages into highly rated securities and sold them wholesale to unsuspecting insurance companies and pension funds, while betting with credit default swaps that they would fail. With the US housing collapse, GS was the only major investment bank which escaped losses. Of course, the US Treasury and the financial regulators were all populated with GS alumni, who were ready to rescue GS and the rigged system.

In the GFC, trillions of dollars of bail-out were injected into the banks to stabilize the financial system, supposedly to forestall another Great Depression. Instead of anyone responsible for the investment bank debacles going to jail for fraud or misconduct, the senior managers got increased bonuses, with the CEO of GS, Lloyd Blankfein eventually joining the billionaires’ club in 2015, for “doing God’s work”.

In a television interview, a journalist asked the US president, why the US Department of Justice did not investigate criminal wrong-doing in relation to the mortgage crisis, Barack Obama replied that “they did nothing illegal”, thus pre-empting the course of justice. This confirms what is already self-evident that the financial industries, particularly the banks, have been allowed, through a rigged legal system, to plunder private property, as warned by John Taylor’s insightful observation.

The main reason for discussing systemic plunder is our observation that macroeconomics cannot be understood without an autonomous sector in the institution of government. The mainstream assumption of methodological individualism cannot possibly lead to valid or useful models because models of individual behaviour alone cannot explain a real economy where wealth and resource distribution are strongly influenced by the government rigging the legal system. For example, the wealth accumulated in the financial sector is mostly unrelated to real economic consumption and production, but due largely to plunder in a rigged legal system.

Laws from Boiling Frog

The interesting question is: how the laws could be changed in a democracy, against the interest of most people, without much political resistance? A hint comes from one of the most powerful bureaucrats in the world, Jean-Claude Juncker, the President of the European Commission, when he was asked how the creation of the European Union was made possible, with so many potential obstacles. The modus operandi of this process is well summarized (Charlemagne, 2002) by his remark:

We decide on something, leave it lying around, and wait and see what happens. If no one kicks up a fuss, because most people don't understand what has been decided, we continue step by step until there is no turning back.

Essentially, what Juncker was explaining is that something as improbable as the European Union could be created by applying the “boiling frog” principle to government legislation. By a sequence of apparently innocuous legislative amendments, which most ignorant politicians do not understand, significant laws can eventually be passed without much resistance. Only when the laws are applied and tested do the public eventually understand the serious ramifications of what they have allowed to come to pass.

It is important to note that this process of incremental change in legislation only works in a democracy “if no one kicks up a fuss” at any step in a sequence. Hence, it is the burden and responsibility of every citizen who understands the devious implications of any legislative amendment to “kick up a fuss”, simply on the principle that if it is wrong it could have future ramifications, even if it may not appear to matter much at the time. Important examples of the need to “kick up a fuss” happened recently with proposed changes to the regulation of Australian superannuation funds.

Plunder of Pension Savings

At over two trillion dollars in total assets, Australian superannuation funds represent mandatory and voluntary retirement savings of most workers. This honey-pot offers an irresistible target for systemic plunder. The previous post shows how the Australian government and the superannuation regulator are attempting to reform MySuper default system, by changing the existing way that blue-collar worker contributions are directed predominantly to Industry funds [1]. So far, Industry funds have been very successful in protecting the workers’ savings from predation. However, the workers’ savings mostly invested in MySuper default funds amount substantially to about one quarter of the total assets of the system. Since MySuper is too well protected from easy systemic plunder, the financial services industry must have it changed by legislation.

This post describes another example in Australian superannuation, where legislative amendment is also designed to facilitate systemic plunder. It was proposed to the Australian Parliament in November 2017 to require all institutional funds to have at least one-third independent trustee directors, which sounds fine until one investigates what “independent” means. The intention of the amendment is to force professional money managers onto the board of Industry funds [1]. The consequence of the change is to allow bankers and other service providers to be trustee directors to more easily and legally plunder the retirement savings of Australian workers.

Enclosed below is a submission to the Senate Economic Legislation Committee to expose the flaws in the proposed legislation to alter the governance requirements of superannuation funds, and particularly Industry funds. This and also similar efforts by others in “kicking up a fuss” appear to have slowed the process of legal plunder of Australian retirement savings. Representing a temporary victory for vigilantes, just before Christmas 2017, the Government withdrew the bill from the senate, citing insufficient support from non-partisan senators.

Below is the submission which “kicks up a fuss” about how the principles of sound governance may be eroded through legislation to facilitate plunder of pension savings. The way this has been attempted by changing the meaning of a key word serves as a serious warning on the deviousness of the process.

Superannuation Governance: If it ain’t broke…

The current Bill for “strengthening trustee arrangements” before Parliament has a non-standard definition of independence which prevents the alignment of interests between directors and members of superannuation. This alignment of interests with members is good governance because it reduces conflicts of interests. Since the Bill proposes a concept of independence which is bad governance and it is potentially harmful to superannuation, Parliament should reject it.

The current Government seems to be doing its best to destroy Australian superannuation. Since the Wallis inquiry in 1996, nearly twenty years of performance data show that Industry funds [1] performed, on average, more than two percent per annum better than Retail funds [2] – a significantly better result. Nevertheless, the Government seems impelled to change how Industry funds are run, at the behest of the lobbyists of the $147 billion financial services industry.

The governance model of Industry funds are similar to those of the best performing pension funds in the world, for example, those of The Netherlands, Denmark and Canada. Yet when David Murray, a former CEO of the Commonwealth Bank and the chair of the 2014 Financial System Inquiry (FSI) was interviewed in October 2017 on why the best governance model needs to be changed, he said:

In my view that is not a sufficient condition, independence and skill set are more important.

By asserting that the best model is insufficient, David Murray has ignored the fact that Retail funds, with a commercial model, supposedly having the greatest independence and skill set, have performed worst and relatively poorly against other funds, not to mention being convicted of numerous crimes and subjected to various scandals. The facts contradict David Murray’s theory. The Government’s rationale for legislative changes appears to have little scientific basis. On Industry fund governance, the Government seems to be saying:

It works very well in practice, but it doesn’t work in theory. If the facts do not fit the theory, then change the facts.

Reforming superannuation governance is how the Government is going to change the facts. However, could it be that the theory is wrong or the theory is misunderstood?

According to current government policy of economic rationalism, Industry funds are not driven by the need to make profit in the market, therefore they cannot possibly be competitive or efficient like Retail funds are expected to be. However, facts have contradicted theory dramatically in the global financial crisis (GFC), and more generally and persistently in Australian superannuation and many other economic situations.

Independence

In the Bill for “strengthening trustee arrangements”, before Parliament, the Government has proposed that superannuation board should be legally required to have one-third independent directors and an independent chair, as Rowell (2017) explained the position of the Government and the Australian Prudential Regulation Authority (APRA):

…some comment on the Government’s proposed legislative amendments to require a minimum of one-third independent directors and an independent chair on superannuation boards APRA’s position on the value of having independent directors on boards remains unchanged.

Directors are to be independent from what? Without clearly defining what is meant by independent, the Government has conflated two different ways in which director independence is used in public discussion. To avoid muddled thinking, we define the two different concepts for independent director in Australian superannuation as follows.

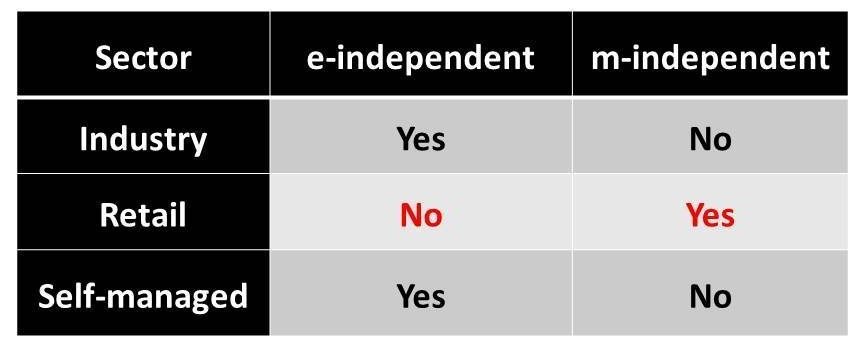

An e-independent director is one who has no relationship with executives, employees, investment managers or service providers of the fund.

An m-independent director is one who is not related to the fund, is not a member of the fund, and is not a member of an organization which represents members of the fund.

The concept of director independence in corporate law is same as the definition of e-independence given here. Good corporate governance requires board directors to protect the interests of minority shareholders against potentially predatory actions by executives. Independence refers normally to what we are calling in this paper e-independence and it is widely accepted as desirable and is enshrined in Section 181 of the Corporations Act 2001.

The e-independence definition has recently been reaffirmed by the Australian Securities and Investment Commission (ASIC, 2017) in a stricter application of the restricted use of the word, independent under Section 923A of the Corporations Act 2001, relating to when financial advisors could claimed that their businesses are “independently owned”. The definition of e-independence should apply uniformly and consistently across all entities regulated by ASIC or APRA, but this consistency will be prevented by the proposed Bill.

Directors of Industry funds are e-independent because generally they have no direct relationships with the executives or service providers of their funds. On the other hand, many directors of Retail funds, particularly those directors related to financial conglomerates, are not e-independent, because Retail fund directors are often also directors or executives of the service providers of their funds. This situation creates conflicts of interest.

In an official survey (Sy et al., 2008), it was found that nearly 60 percent of Retail board directors have one or more associations with fund service providers, about three times greater on average than those in the non-profit sectors. Also, on average, Retail directors have seven simultaneous directorships, about three times as many as Industry fund directors. More recently, Liu and Ooi (2017) [3] have confirmed that Retail funds outsource to service providers which are predominately related parties.

Conflicted directors could make decisions which profit their related service providers at the expense of members of their own superannuation funds (Liu and Ooi, 2017) [3]. Despite the greater investment skill set of Retail directors, the empirical evidence on the poor investment performance of Retail funds suggests that the lack of e-independence has been harming members of Retail funds. Hence in accordance with good corporate governance,

Directors of superannuation funds should be e-independent, with no relationships with the service providers of their funds.

However, instead of using e-independence as the definition of independence, the financial services industry, the Government and APRA have made a confusing switch and used m-independence as the definition of independence. That is, the standard meaning of independence has been replaced by a different meaning of independence without clear warning or justification. The Government simply assumes that m-independence, and only m-independence, is good governance.

The Senate Economics Legislation Committee (SELC, 2015) has noted the Dissenting Report by Labor Senators who have objected to the conflation of the two different models of governance. It should be re-iterated and emphasized here that

The conflation of e-independence with m-independence is unhelpful for the formulation of sound governance policy in Australian superannuation.

Alignment of Interests

More clearly stated, the Government has proposed (Rowell, 2017) that superannuation board should have at least one third directors who are m-independent, which is inconsistent with the meaning of independent when applied to the directors of other APRA regulated entities. Is m-independence or non-alignment of director interests with those of their beneficiaries, a good thing for superannuation governance?

The implicit assumption is that there should be a sufficient number of directors who are not members or do not represent members of their funds, because m-independence or non-alignment of interests is assumed somehow necessary for good governance. This idea goes against the experiences of the whole financial services industry. For example, corporations typically issue their directors and executives with shares so that their interests are aligned with those of their shareholders.

Similarly, most money managers (e.g. Warren Buffett) take great pains to convince their investors that they have “skin in the game” by managing all their own money alongside their clients in a comingled fashion to demonstrate a total alignment of interests. That is, they are showing that they are managing other people’s money as their own. By declaring that m-independence is necessary for good governance, APRA is indirectly asserting that total alignment of interests is bad governance. To emphasize,

If alignment of interests of directors with those for whom they serve is good governance, then by implication m-independence is bad governance.

For example, Retail fund directors may approve paying high fees to associated service providers, something which they would not have done if their own retirement savings were also in the fund. Clearly, from a member’s point of view, m-independent directors are undesirable. Retail directors are mostly m-independent.

Retail directors not aligned with the interests of their members pose the greatest risk to the retirement savings of those members. Only about 21 percent of Retail directors are members of the funds of which they are directors. On average, only 12 per cent of their personal superannuation assets are in those funds. The correspondence figures for the directors of other funds are 62 to 73 percent and 44 to 63 percent respectively (Sy et al., 2008).

Apart from Retail funds, most Australian superannuation funds are not m-independent; that is, their directors have substantial alignment of interests. Table 1 shows how funds from different sectors are classified according to the two definitions of director independence.

Table 1: Director Independence

On average, Retail funds have performed worse than funds in the non-profit segment (Sy, 2017) [4]. Therefore, the empirical evidence shows that m-independence has not helped Retail funds to deliver good performance results. Instead, high or total alignment of interests in Industry funds and Self-managed superannuation funds has helped, certainly not harmed, their performances. With neither theoretical nor empirical justification,

It is questionable whether m-independence has any relevance to good governance of Australian superannuation funds.

In the same interview, Jeremy Cooper, the chair of the 2010 Super System Review (SSR), took the idea of alignment of interest even further. He suggested that there should be many more 80-year-old directors because in future, superannuation funds will be run to provide income streams for those who have long retired. This suggestion is entirely consistent with the principle that good governance should involve alignment of interests.

Instead of m-independence, on the contrary, an abundance of research has shown that e-independence is important in corporate governance. Yet the Government has substituted for e-independence with an unproven and potentially harmful m-independence. Retail funds are not e-independent and yet they are not the focus of governance reform in Australian superannuation when they should be.

Investment Skills

Echoing David Murray’s remarks, Rowell (2017) continued the above quotation by saying that investment skills were the common rationale for independent directors:

As I indicated in this forum back in 2015, independent directors broaden the skills and capabilities that can be brought to the board table, and improve decision-making by bringing an objective perspective to issues the board considers.

An implicit assumption in this statement is that skills and capabilities can be brought to the board only if directors are objective by being m-independent or have non-alignment of interests. This belief can be challenged by the evidence.

Retail fund directors generally have higher educational qualifications, more hands-on work experience in the financial services industry and presumably a greater investment skill set than directors in other sectors (Sy et al., 2008). However, the empirical evidence shows that this advantage appears irrelevant and even counter-productive in delivering benefits to the members of Retail funds. There are several possible reasons for this.

The first reason, which is rarely mentioned, is that the lack of investment skills at the level of superannuation board matters far less than it appears because board directors are rarely involved directly in investing. Superannuation boards generally have sufficient resources to hire asset consultants for advice on portfolio design, for implementation and for performance monitoring. What matters most in a director, is diligence and a genuine concern for the investment performance and operation of their funds.

A certain level of investment knowledge is certainly required of directors but beyond that more investment skills do not necessarily translate to better investment performance for the funds. Choosing the right advisors who choose the right investment managers making the right decisions is how superannuation funds are normally expected to discharge their fiduciary duty. As on other corporate boards, superannuation directors are generally not fund executives but watchdogs who monitor and supervise executive performance.

A much more important reason for poor performance is the lack of e-independence of Retail directors who, as mentioned above, are often related to service providers of their funds. The conflicts of interests often resolve in favour of related service providers at the expense of members who merely rely on the honesty of directors to do their fiduciary duty, under Section 52 of the Superannuation Industry (Supervision) Act 1993.

Conflicts of Interest

Continuing further with the above quotation, Rowell (2017) asserts that independent directors are well capable of managing conflicts of interest:

They are also well-placed to hold other directors accountable, particularly in relation to conflicts of interest. This is as relevant for directors of industry and other not-for profit funds that may face potential conflicts with the interests of their stakeholders (such as nominating organisations), as it is for directors of retail funds.

Again, the facts contradict this assertion because Retail funds have mostly m-independent directors. Yet, over long periods, Retail funds have under-performed other funds significantly, consistently and persistently. Moreover, more than other types of funds, Retail funds have had numerous scandals with fines and convictions which are sufficient to be reported by the financial media.

In fact, it is highly unlikely that m-independent directors are capable of managing their own conflicts of interest, let alone those of others. Directors who have significant investment skills are likely to have multiple directorships simultaneously as shown by official data (Sy et al., 2008). They are therefore unlikely to be e-independent as required by the Corporations Act 2001. To emphasize,

Directors with high investment skills are more likely to have significant conflicts of interest, because they usually have multiple directorships, some of which are likely to be with service providers.

Even an m-independent director with only a single directorship of a superannuation fund does not itself guarantee freedom from conflict, because the director could be induced to make decision favourable to an interested party at the expense of members of the fund. For example, an employer may be induced by cheap business loans offered by a financial conglomerate to choose a Retail fund which may be against the interests of their own employees. Financial advisors are m-independent and yet through kick-backs, trailing commissions and other inducements, some of them have acted against the interests of their own clients.

It was not any actual issues of conflicts of interest which attracted the Government’s attention on the governance of Industry funds. Rather, the various Government inquiries, e.g. SSR and FSI, implicitly noted potential issues in the way Industry fund directors are elected. The main concern relates to the power of the trade unions to elect directors: whether the directors are appointed on skills and merit or whether they are appointed as reward for successful careers in the trade unions.

The real issue is more about whether the directors are fairly and appropriately elected and less about whether the interests of members have been damaged. Clearly, it is desirable to have a fairer process based on merit rather than favouritism and the potentially corrupt processes may need to change. This is a problem which the anti-corruption regulators and the trade unions themselves should address, but it is not a problem which could be solved appropriately by legislating for m-independent directors.

However defective may be the process of electing directors, the empirical evidence suggests that the interests of members of Industry funds have not been damaged. The reason is: the losses from questionable spending by sinecure directors pale in comparison to the losses arising from conflicts of interest which could result in many billions of Retail savings being diverted to the financial services industry.

In 2017, CBA group reported $9.9 billion annual profit, with about a quarter of this profit coming from $5.5 billion of income from providing services in funds management, market dealing and related institutional banking. The superannuation funds of large conglomerates have been looted for profit, operating some of the worst performing funds in the industry (Sy, 2017) [4].

In the above mentioned interview, a journalist asked why some of the largest companies in Australia have had independent directors for years and yet have been involved in law breaking and misbehaviour. David Murray replied:

That may be the case, but I don’t see how that can be related to the objects of a good design. You can have a good design and a problem.

Any design manifestly having many problems arising from conflicts of interest and misbehaviour is, by definition, not a good design. A good design should not have many instances of misbehaviour as has been the case with Retail funds. Clearly, the evidence on best practice has shown,

The best defence against the problems of conflicts of interests is the solution of alignment of interests. This solution is prevented by the proposed legislation to have m-independent directors.

An independent director in superannuation should be defined simply as a director who is free from conflicts of interest which could damage the welfare of members.

Conclusion

In superannuation governance, the Government has changed the meaning of independent from one (e-independent) which is widely acknowledged as desirable to one (m-independent) which is undesirable. To put this simply, for superannuation, e-independence is good governance which the Government ignores, while m-independence is bad governance which the Government wants to enshrine in legislation.

The call for independent directors in superannuation by the Government is therefore a piece of casuistry, because politicians and the public may not be aware that the meaning of independent is different from what they normally understand. In a moment of carelessness or hurry, the Bill could be passed by Parliament giving APRA unwarranted discretionary powers (Schedule 1, Part 9, Section 90(1)) to determine

…that a person is not independent from an RSE licensee if APRA is reasonably satisfied that the person is unlikely to be able to exercise independent judgement in performing the role…

Being independent from a responsible superannuation entity (RSE licensee) is by definition being m-independent from a superannuation fund. To exercising independent judgement means to exercise judgement independent of the interests of members of the superannuation fund. This m-independence is undesirable for the performance of the fiduciary duty of Section 52 of the Superannuation Industry (Supervision) Act 1993. The proposed legislation is therefore against the interests of the members of superannuation funds. The proposed legislation has the effect of making the governance of Industry funds more like that of Retail funds: a retrograde step, allowing the camel’s nose in the tent.

The current Government seems to be doing its best to destroy Australian superannuation. The Bill for “strengthening trustee arrangements” actually weakens superannuation governance and therefore should be rejected by Parliament. Instead, the Bill should be amended so that the definition of independence for superannuation is e-independence, consistent with that of the Corporations Act 2001.

Endnote

[1] An Industry fund is a non-profit organization managing the superannuation portfolios of its mutual members.

[2] A Retail fund is a commercial organization managing to make profits for its shareholders by selling superannuation products to its members, as consumers.

[3] Liu, K. and Ooi, E. (2017), “The impact of related-party outsourcing and trustee director affiliation on investment performance of superannuation Funds”, Report to Industry Super Australia, (to be published).

[4] Sy, W. (2017), “Impact of asset allocation and operational structure on the investment performance of Australian superannuation”, Report to Industry Super Australia, (to be published).

For other sources see References and citations

Your definition of Capitalism begs the question as to what is the capital being owned and used? Many years ago, after Adam Smith and other classical economists told us what capital really was a certain interfering and biased economist named John Bates Clark, along with his friends and in collaboration with the monopolists of the time (about 1900) claimed that capital includes both durable capital goods and land. Previously it was shown that LAND IS NOT CAPITAL, but this inconvenient truth allowed the way landlords monopolized and exploited the ownership of land, by speculation in its growing value, to be hidden and for land being withheld from use to be ignored.

The 3 Smithian factors of production, Land , Labor and Capital are as true today as when they were first exposed about 240 years ago, but modern economists choose to combine the first and last ones into a single quantity and thereby confuse our understanding of the whole social system of macroeconomics. It is high time this situation was righted and we appreciate that when a change happens to our social system that the performance and response of durable capital goods (capital) and of natural resources (land) are completely different.

By correcting our definitions do we stand a chance of clear thinking and gained knowledge about how our social system works. My recent book "Consequential Macroeconomics" on this subject is available for free as an e-copy--write to me at chesterdh@hotmail.com to get it, and blow away all those "dismal" cobwebs of the older and decrepit theories!

http://www.asepp.com/definitions/

Capital is the means of production including resources, technology, knowledge, goods and services which are useful for production.

Hi Wilson. It has been some time since I have been able to read and comment. Very useful difference between inequality and inequity, something which I can say I have kept fairly clear in my own mind. I do not have much time right now, but this piece is in a similar vein to Bill Black's work on financial fraud in the United States. I will have more to say later.